Please refer to important disclosures at the end of this report

1

Aster DM Healthcare Ltd (ADHL) is one of the largest private healthcare service

providers which operates in multiple GCC states and is an emerging hea

lthcare

player in India. ADHL

operates in all of the GCC states (UAE, Oman, Saudi Arabia,

Qatar, Kuwait, Bahrain and Jordan), India and the Philippines.

The company operates in multiple segments of the healthcare s

ervices industry,

including hospitals, clinics and retail pharmacies. As of September 30, 2017, the

Company had 17,408 employees including 1,417 full time doctors, 5,797 nurses,

1,752 paramedics, and 8,442 other employees (including pharmacists). GCC

operations are headquartered in Dubai, UAE, while

Indian operations are

headquartered in Kochi, Kerala.

Positives: (a) Diversified revenue sources from hospitals, clinics and pharmacies

(b)

Long standing presence with established brand equity and positioning (c)

Ability to

attract and retain high quality medical professionals (d) Experienced c

ore

management team

Investment concerns:

(a) In 1HFY2018, the company’s 81% revenue came from

GCC region and balance from India, reflecting geographical concentration ri

sk (b)

Despite strong revenue CAGR of ~24% over FY15-

17, ADHL has seen fluctuation

in profitability and reported loss in 1HFY18 due to instability in operating margins

(c) In the past, the company has suffered losses from Sanad Hospital, Saudi Arabia

which

had higher exposure in revenue from government, however the company

has reduced the revenue exposure from 82% in FY16 to 38% in FY17.

Outlook & Valuation: In terms of valuations, the pre-

issue EV/EBITDA works out to

32.5x its 1HFY2018 annualized EBITDA (a

t the upper end of the issue price band),

which is higher compared to its peers like Apollo Hospitals Enterprise (

trading at PE

22.3x -1HFY2018 annualized EBITDA). On EV/ Bed basis, ADHL is `2.4cr vs

Apollo Hospitals Enterprise’s `1.7cr. Further, last thre

e years’ financial

performance including 1HFY18 numbers doesn’t provides confidence.

Hence, we

recommend Neutral rating on the issue.

Key Financials

Y/E March (` cr)

FY2015 FY2016

FY2017

1HFY18

Net Sales 3,876 5,250

5,931

3,123

% chg - 35.5 13.0

-

Net Profit 272 8

267

(83)

% chg - (97.0) 3,148.7

-

OPM (%) 13.1 8.5 5.6 5.7

EPS (Rs)

6.7

0.2 6.6

(2.1)

P/E (x) 28.2 933.0 28.7

-

P/BV (x) 3.4 12.8 3.4

-

RoE (%) 12.1 1.4 11.9

-

RoCE (%) 11.5 5.4 0.2

-

EV/Sales (x) 2.1 2.0 1.7

-

EV/EBITDA (x) 16.1 23.4 30.3

-

Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end

of the price band

Neutral

Issue Open: Feb 12, 2018

Issue Close: Feb 15, 2018

QIBs 50% of issue

Non-Institutional 15% of issue

Retail 35% of issue

Promoters 37.4%

Others 62.6%

Post Issue Shareholding Pattern

Post Eq. Paid up Capital:

`505

cr

Issue size (amount): **

`980

cr (Inculde

offer for sale -

`255

)

Price Band:

`180

-190

Lot Size: 78 shares and in multiple

thereafter

Post-issue implied mkt. cap: *

`9,094

cr

- **

`9,599

cr

Promoters holding Pre-Issue: 43.3%

Promoters holding Post-Issue: 37.4%

*Calculated on lower price band

** Calculated on upper price band

Book Building

Fresh issue:

`725

cr

Issue Details

Face Value:

`10

Present Eq. Paid up Capital:

`467

cr

Amarjeet S Maurya

+022 39357600, Extn: 6831

amarjeet.maurya@angelbroking.com

Aster DM Healthcare Ltd

IPO Note | Healthcare

Feb 08, 2018

Aster DM Healthcare Limited |

IPO Note

Feb 08, 2018

2

Company background

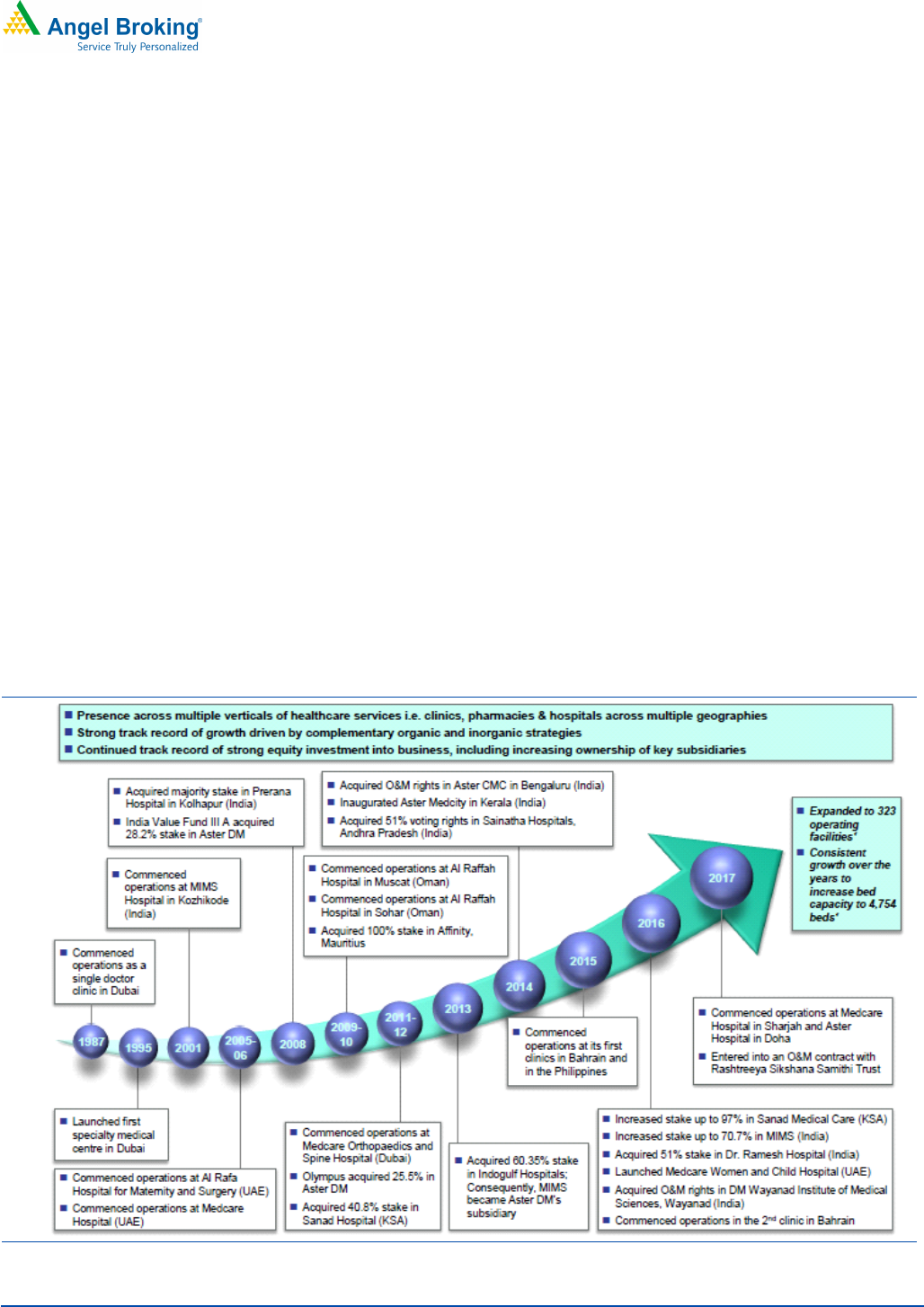

Incorporated in 1987, Aster DM Healthcare Ltd is Kochi, Kerala based healthcare

service provider with operations in GCC states (United Arab Emirates, Oman,

Saudi Arabia, Qatar, Kuwait and Bahrain), India and the Philippines. Company’s

Indian operations are headquartered in Kochi, Kerala.

Aster DM Healthcare operates in multiple segments of the healthcare industry

including hospitals, clinics and retail pharmacies. Company operates hospitals and

clinics, pharmacies, diagnostic centers, educational institutions, healthcare

management and healthcare support systems. Company provides healthcare

services to patients across economic segments under brand names including

"Aster", "Medcare" and "Access".

Aster's healthcare facilities consists of 9 hospitals, 90 clinics and 206 retail

pharmacies in the GCC states, 10 multi-specialty hospitals and 7 clinics in India,

and 1 clinic in the Philippines as of September 30, 2017. Aster's had 17,408

employees as of September 30, 2017, including 1,417 full time doctors, 5,797

nurses, 1,752 paramedics and 8,442 other employees (including pharmacists).

Aster's hospitals in India are located in Kochi, Kolhapur, Kozhikode, Kottakkal,

Bengaluru, Vijayawada, Guntur, Wayanad and Hyderabad, and are generally

operated under the Aster, MIMS, Ramesh and Prime brands.

Exhibit 1: Evolution of Aster DM

Source: Company, Angel Research

Aster DM Healthcare Limited |

IPO Note

Feb 08, 2018

3

Issue details

ADHL’s IPO is a mix of offer-for-sale and fresh issue of shares. The issue would

constitute fresh issue of shares worth `725cr, with offer-for-sale of 1.3cr shares.

The company will dilute 7.6% of its post-offer paid-up equity share capital.

Exhibit 2: Pre and Post-IPO shareholding pattern

(No. of share) Pre-Issue

(%)

Pre-Post

(%)

Promoters

202,134,341

43.3%

188706090

37.4%

Others

264,935,110

56.7%

316521256

62.6%

467,069,451

100.0%

505227346

100.0%

Source: Source: RHP, Note: Calculated on upper price band

Objects of the offer

The objects of the Offer for the Company are to:

Repayment and/or pre-payment of debt (`564cr)

Purchase of medical equipment (`110cr); and

General corporate purposes

Key Risk

Aggressive expansion plan would improve the revenue visibility which can

pose upside risk

Higher attrition of reputed doctors can have an impact on the financials

Increase in competition from other players can impact the business of

company

High geographical concentration in GCC countries which can increase

risks for company

Aster DM Healthcare Limited |

IPO Note

Feb 08, 2018

4

Consolidated Income Statement

Y/E March (` cr) FY2015 FY2016 FY2017

1HFY18

Total operating income 3,876 5,250

5,931

3,123

% chg - 35.5 13.0

-

Total Expenditure 3,370 4,804

5,599

2,944

Raw Material 1,222 1,623

1,887

973

Personnel 1,154 1,629

2,055

1,128

Others Expenses

994

1,552

1,657

844

EBITDA

506

446

332

178

% chg - (11.9)

(25.5)

-

(% of Net Sales) 13.1 8.5 5.6 5.7

Depreciation& Amortization

144

243

322

174

EBIT

362

203

10 5

% chg - (44.1)

(95.2)

-

(% of Net Sales) 9.3 3.9 0.2 0.1

Interest & other Charges 79

189

354

89

Other Income 23 25 37

19

(% of PBT) 7.6 67.2 12.7

(28.4)

Exceptional Items -

-

596.1

-

Share in profit of Associates

0 (1) (0) (0)

Recurring PBT

306

38

289

(66)

% chg (87.7) 666.8

-

Tax 34 29 22

17

(% of PBT) 11.2 78.2 7.6

(25.0)

PAT (reported) 272.1 8.2

266.7

(82.7)

% chg - (97.0) 3,148.7

-

(% of Net Sales) 7.0 0.2 4.5 (2.6)

Basic EPS (`)

6.7

0.2

6.6

(2.1)

Fully Diluted EPS (`)

6.7

0.2

6.6

(2.1)

% chg (97.0) 3,148.7

Source: RHP, Angel Research

Aster DM Healthcare Limited |

IPO Note

Feb 08, 2018

5

Consolidated Balance Sheet

Y/E March (` cr)

FY2015

FY2016 FY2017

1HFY18

SOURCES OF FUNDS

Equity Share Capital

389

403

403

403

Reserves& Surplus

1,857

194

1,847

1,774

Shareholders Funds

2,246

597

2,251

2,177

Total Loans

901

3,162

2,807

2,957

Deferred Tax Liability

135

156

169

170

Total Liabilities

3,282

3,914

5,227

5,304

APPLICATION OF FUNDS

Net Block

1,785

2,037

2,767

2,966

Capital Work-in-Progress

197

358

290

233

Investments

3

39 22

26

Goodwill

452

470

753

750

Current Assets

1,965

2,822

2,936

3,072

Inventories

311

411

526

543

Sundry Debtors

884

1,342

1,288

1,488

Cash

304

267

152

127

Loans & Advances

-

-

-

-

Other Assets

465

802

971

914

Current liabilities

1,130

1,842

1,581

1,790

Net Current Assets

835

980

1,355

1,282

Deferred Tax Asset

10

30 40

47

Total Assets

3,282

3,914

5,227

5,304

Source: RHP, Angel Research

Aster DM Healthcare Limited |

IPO Note

Feb 08, 2018

6

Consolidated Cash Flow Statement

Y/E March (` cr)

FY2015

FY2016 FY2017 1HFY2018

Profit before tax

306

38

(307)

(66)

Depreciation

144

243

322

174

Change in Working Capital

(490)

(681)

(154)

(89)

Interest / Dividend (Net)

0

7 0 0

Direct taxes paid

(22)

(34)

(44)

(22)

Others

298

629

549

126

Cash Flow from Operations

236

203

366

123

(Inc.)/ Dec. in Fixed Assets

(395)

(744)

(925)

(201)

(Inc.)/ Dec. in Investments

(53)

(42)

(228)

(56)

Cash Flow from Investing

(448)

(786)

(1153)

(257)

Issue of Equity

(395)

(744)

(925)

(201)

Inc./(Dec.) in loans

212

2422

876

155

Dividend Paid (Incl. Tax)

(17)

(49)

(16)

(7)

Finance charges paid

(80)

(89)

(174)

(92)

Others

482

(961)

887

202

Cash Flow from Financing

203

578

648

56

Inc./(Dec.) in Cash

(10)

(5)

(138)

(79)

Effect of exch diff on cash

9

10 16 (0)

Opening Cash balances

248

248

253

131

Closing Cash balances

248

253

131

52

Source: Company, Angel Research

Aster DM Healthcare Limited |

IPO Note

Feb 08, 2018

7

Exhibit 3: Key Ratios

Y/E March FY2015

FY2016

FY2017

Valuation Ratio (x)

P/E (on FDEPS)

28.2

933.0

28.7

P/CEPS

18.4

30.5

13.0

P/BV

3.4

12.8

3.4

Dividend yield (%)

0.0

0.0

0.0

EV/Sales

2.1

2.0

1.7

EV/EBITDA

16.1

23.4

30.3

EV / Total Assets

2.5

2.7

1.9

Per Share Data (Rs)

EPS (Basic)

6.7

0.2

6.6

EPS (fully diluted)

6.7

0.2

6.6

Cash EPS

10.3

6.2

14.6

Book Value

55.7

14.8

55.8

Returns (%)

ROCE

11.5

5.4

0.2

Angel ROIC (Pre-tax)

13.2

6.1

0.2

ROE

12.1

1.4

11.9

Turnover ratios (x)

Inventory / Sales (days)

29

29

32

Receivables (days)

83

93

79

Payables (days)

41

48

48

Working capital cycle (ex-cash) (days)

72

73

63

Source: Company, Angel Research

Aster DM Healthcare Limited |

IPO Note

Feb 08, 2018

8

Research Team Tel: 022

-

39357800 E

-

mail: research@angelbroking.

com Website:

www.angelbroking.com

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and investment advisor with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.